A deep dive into the 6 big simplifications in the new ESRS

Our analysis looks at what has changed and how it will impact your reporting going forward

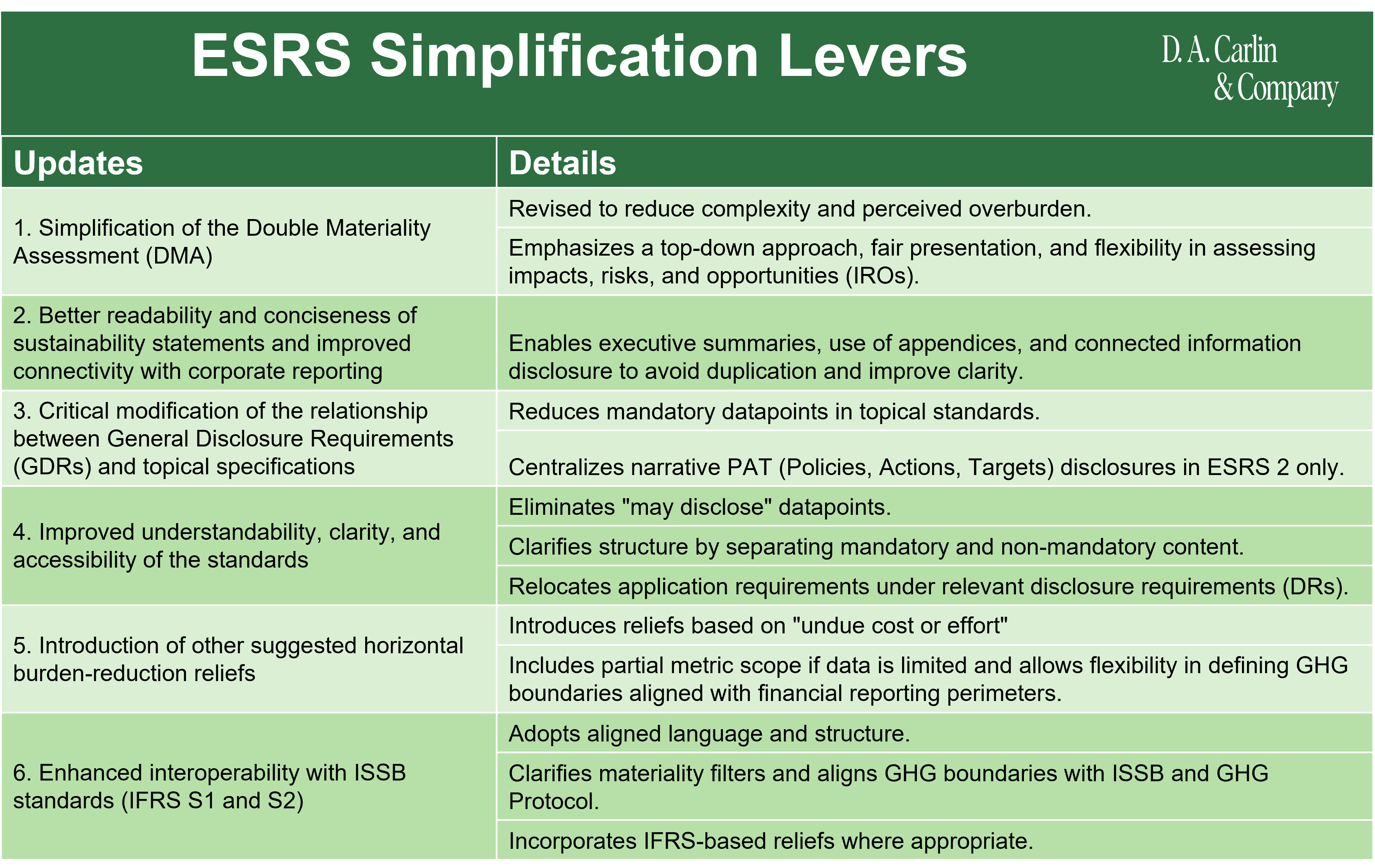

For firms preparing to comply with the EU’s Corporate Sustainability Reporting Directive (CSRD), the European Financial Reporting Advisory Group (EFRAG) has just released a major proposed update to the European Sustainability Reporting Standards (ESRS). The draft revisions, reduce mandatory datapoints by 57% and eliminate all voluntary disclosures, cutt…

Keep reading with a 7-day free trial

Subscribe to David Carlin's Digest: Your Guide to a Changing World to keep reading this post and get 7 days of free access to the full post archives.